by Mike Lynch, Managing Director of the Hartford Funds Applied Insights Team

Understand the benefits a spouse (or former spouse) may be entitled to receive in four scenarios.

For many, the rules regarding Social Security benefits are unclear, particularly when it comes to spousal benefits. Making matters more challenging is the fact that the rules aren’t the same for those who are married, widowed, or divorced. These examples can help clarify some of the confusion using four scenarios.

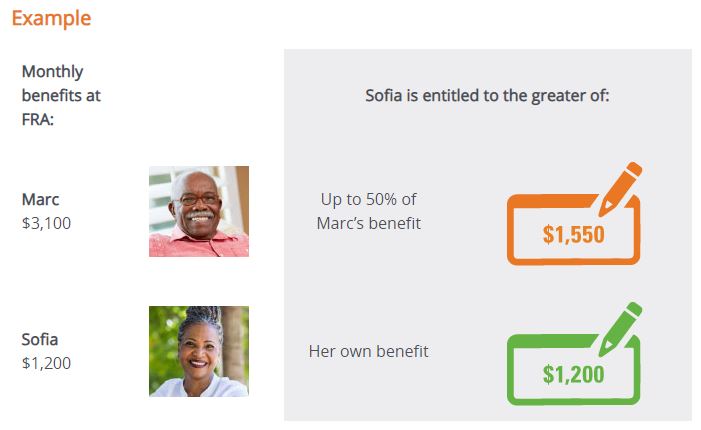

1. Spousal Benefits for Married Couples1

Spouses are entitled to the greater of:

- Their own benefit

- The spousal benefit

- The maximum spousal benefit is up to 50% of the higher earner’s benefit and capped at their full retirement age (FRA) benefit amount

General guidelines:

- A couple must be married for at least one year

- The spousal benefit can’t be claimed until the higher-earning spouse files

- A spouse is entitled to the greater of their individual benefit or the spousal benefit, but not both

- Like individual benefits, spousal benefits can be collected at age 62. But that’s considered early filing (i.e., before FRA) and may potentially reduce the spousal benefit amount.2,3

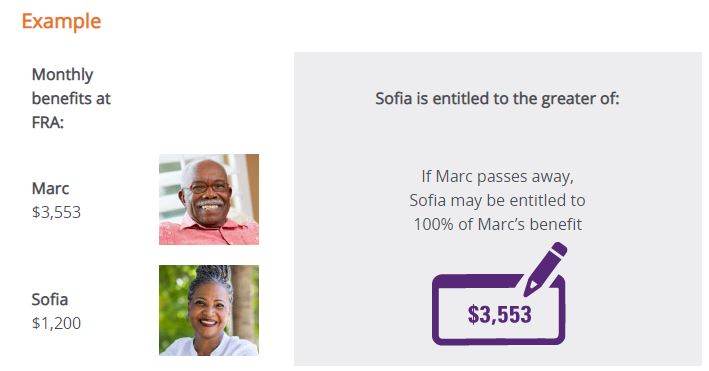

2. Survivor Benefits for Widowed Spouses4

Widowed spouses may be entitled to up to 100% of their deceased spouse’s benefit.

In the case of Marc and Sofia, what would happen if Marc passes away? Instead of continuing to collect 50% of Marc’s benefit, Sofia may be entitled to his full benefit at the time of his death.

General guidelines:

- A couple must have been married for at least nine months

- The surviving spouse must be at least age 60 to begin receiving survivor benefits. But that’s considered early filing (i.e., before FRA) and may potentially reduce the spousal-benefit amount.2,5

- The surviving spouse may be entitled to the greater of: their individual benefit, the spousal benefit, or the survivor benefit

3. Spousal Benefits for Divorced Spouses6

Divorced spouses are entitled to the greater of:

- Their own benefit

- The spousal benefit

- The maximum spousal benefit is up to 50% of the higher earner’s benefit and capped at their full retirement age (FRA) amount

See also: Spousal Benefits for Married Couples illustration in the first scenario.

General guidelines:

- A couple must have been married for at least 10 years and divorced for at least two continuous years

- The lower-earning former spouse who’s filing must be unmarried

- The lower-earning former spouse can file as early as age 62. Again, that’s considered early filing (i.e., before FRA) and may potentially reduce the spousal-benefit amount.2

- The higher-earning former spouse does not need to file first. However, they must be eligible to receive their retirement benefits (i.e., age 62 or older).

- The lower-earning former spouse may need to contact the Social Security Administration (SSA) and provide all necessary documentation if they wish to file for spousal benefits

- If the higher earner remarries, their new spouse may still be eligible to receive spousal benefits. If so, neither the benefit amount for the current spouse nor the former spouse will be affected.

4. Survivor Benefits for Divorced, Widowed Spouses7

If a couple is divorced and the higher-earning former spouse passes away, the surviving former spouse can still claim up to 100% of the deceased former spouse’s benefit.

See also: Survivor Benefits for Widowed Spouses illustration in the second scenario.

General guidelines:

- The surviving former spouse must be age 60 or older3

- The marriage must have lasted for at least 10 years8

- Remarrying before age 60 may make the surviving former spouse ineligible to collect on their deceased former spouse’s record9

- If the former spouse remarries at age 60 or older, they may still be eligible to collect survivor benefits from their deceased ex-spouse’s record

- Benefits paid to a surviving former spouse won’t affect the benefit amounts to which other survivors may be entitled

As you can see, spousal and survivor benefits can provide additional income in retirement. But the rules can be confusing, and the examples provided are relatively basic. As always, we strongly recommend you consult the Social Security Administration for more information. Also, meet with your financial professional, who can help you make the most informed decisions based on your particular situation.

Lynch, M. (2022, May 10). Social Security Benefits for Spouses. Hartford Funds. Retrieved June 10, 2022, from https://www.hartfordfunds.com/insights/investor-insight/client-seminars/social-security/benefits-for-spouses.html?utm_source=hartfordfunds.com&utm_medium=email&utm_campaign=2022-06-06-SUB-SS_Spousal_Benefits&utm_content=investor_insight&programID=8148&mkt_tok=ODYxLVJXUy02OTkAAAGE2SV1U9AH7-vkgmeLCTEEMfx9SE0TCCbHXHCspRfx-xiPvTCyyzT9ToazoY8IpyPrL_LDceLvq4TKzcmXOG4BXZTyWUfWtNyBLEDg2XHnl33GIw