Posted by Lawrence Gillum, CFA, Fixed Income Strategist

Posted by Lawrence Gillum, CFA, Fixed Income Strategist

Tuesday, February 28, 2023

Bond investors experienced the worst year ever for core bonds last year (as per the Bloomberg Aggregate Bond Index), -so the prospects of another year like 2022 could be hard to fathom. The good news is we don’t think we’ll see another year like 2022 anytime soon, but despite the higher starting yield levels, we could see periods of negative returns. In fact, after a strong January for core bonds, unless yields fall dramatically today, February returns will be negative. But that is normal. Since inception of the index in 1975, over a third of the monthly returns have been negative and close to 25% of quarterly returns have been negative. Bonds trade daily and interest rates change throughout the day as well, so that means the market value of a bond will change daily as well.

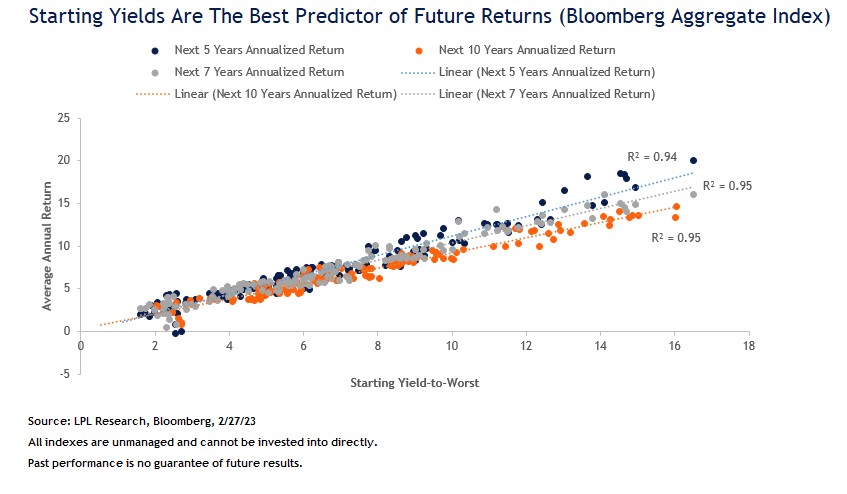

However, fixed income instruments are fundamentally different than other financial instruments. Bonds are financial obligations that are contractually obligated to pay periodic coupons and return principal at or near par at the maturity of the bond. That is, there is a certainty with bonds you don’t get from many other financial instruments—and that is starting yields (yield-to-worst more specifically, which is the minimum expected yield that can be received from a bond absent an issuer defaulting on its debt). Starting yields take into consideration the underlying price of the bond as well as the required coupon payments, therefore, starting yields are the best predictor of future returns. Starting yields and subsequent returns for the Bloomberg Aggregate Bond Index have a very tight relationship. For holding periods as short as five years or as long as ten years, starting yields explain approximately 94% to 95% of returns for the index. That relationship breaks down over shorter periods though with only approximately 40% of 1-year returns explained by starting yields—there is much more variability (noise) over shorter horizons. But if you buy and hold a fixed income investment, the short-term volatility you experience due to changing interest rate expectations is just volatility. It has very little bearing on the actual total return if held to maturity (or if held to the average maturity of a portfolio of bonds).

After the historically awful year for fixed income investors last year, it may be disheartening to see another month (or more) of negative returns. We would advocate for a longer-term perspective though. Current yields within many fixed income markets are at generationally high levels. Investors can take advantage of these high starting yields but only if they stay invested and look past the (normal) short-term volatility that happens on occasion.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors. To determine which investment(s) may be appropriate for you, please consult your financial professional prior to investing.

Investing involves risks including possible loss of principal. No investment strategy or risk management technique can guarantee return or eliminate risk in all market environments. For more information on the risks associated with the strategies and product types discussed please visit https://lplresearch.com/Risks

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Unless otherwise stated LPL Financial and the third party persons and firms mentioned are not affiliates of each other and make no representation with respect to each other. Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

For a list of descriptions of the indexes and economic terms referenced in this publication, please visit our website at lplresearch.com/definitions.

Securities and advisory services offered through LPL Financial, a registered investment advisor and broker-dealer. Member FINRA/SIPC.

Tracking #1-05362051