Posted by George Smith, CFA, CAIA, CIPM, Portfolio Strategist

Posted by George Smith, CFA, CAIA, CIPM, Portfolio Strategist

Wednesday, October 5, 2022

With so much focus on the equity bear market, inflation, interest rates, the Federal Reserve (Fed) and rising recession risks, it’s perhaps no surprise that the buildup to the U.S. midterm elections has taken more of a backseat than in prior election cycles. Given that it is now a little over a month to the election, we wanted to take a closer look at some of our favorite charts relating to midterms, and especially how stock markets have behaved around this point in the Presidential cycle.

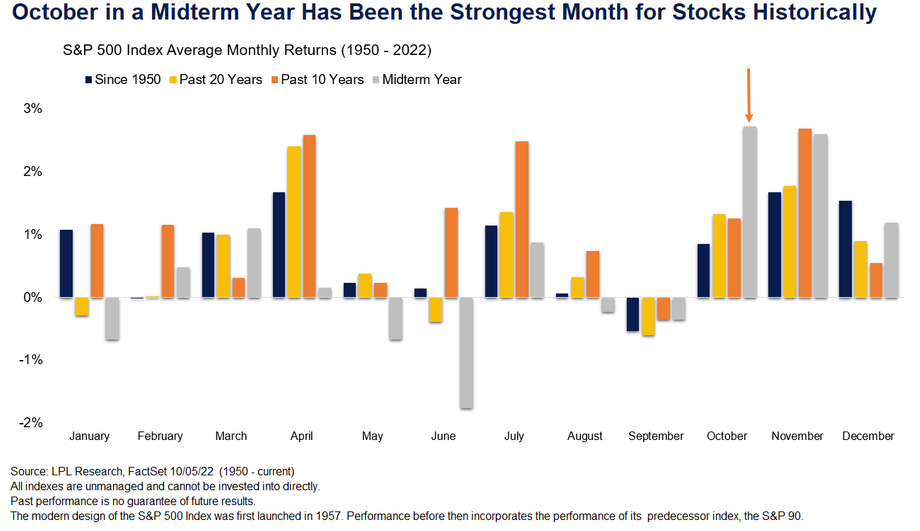

Midterm year seasonality has swung distinctly favorable, with October in a midterm year historically being the strongest month of all for stocks. Stocks have gained an average of 2.7% October in midterm years. The fourth quarter has historically had the strongest seasonality, and it’s especially true in a midterm year, with gains during the final quarter of a midterm year averaging over 6.5%. Directionally this year has played out with a high correlation to the average seasonality for a midterm year with the first half seeing losses, culminating in a big down month in June, followed by a bounce in July, before faltering again in August and September.

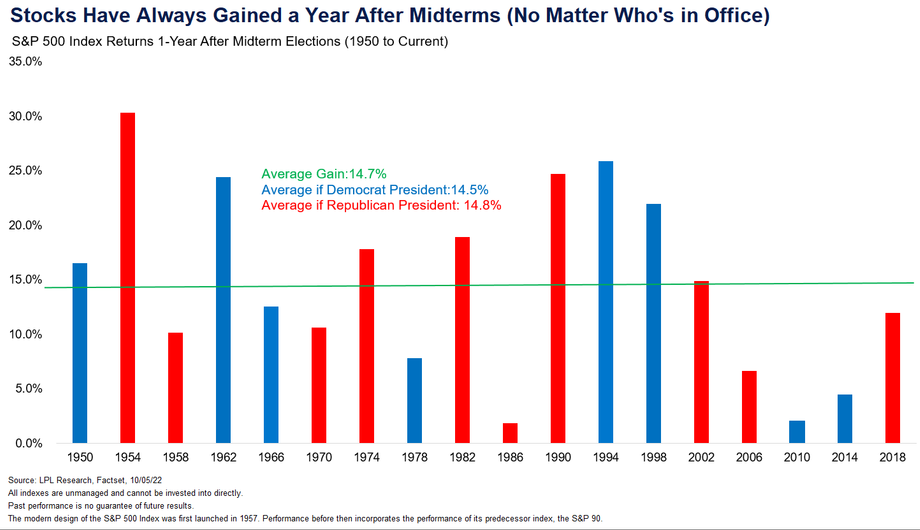

Another favorable historic trend for stocks is looking at returns a year out from the midterm election. Since 1950 stocks have had a positive return one year after the election every time, with an impressive average of almost 15%. We have often said that stock markets tend to be mostly indifferent about the results of U.S. elections (with a split government, and the predictability that gridlock brings, the market’s favorite outcome) and this data is a near perfect example of this. When the average return is broken out by which party is in office, the difference is negligible.

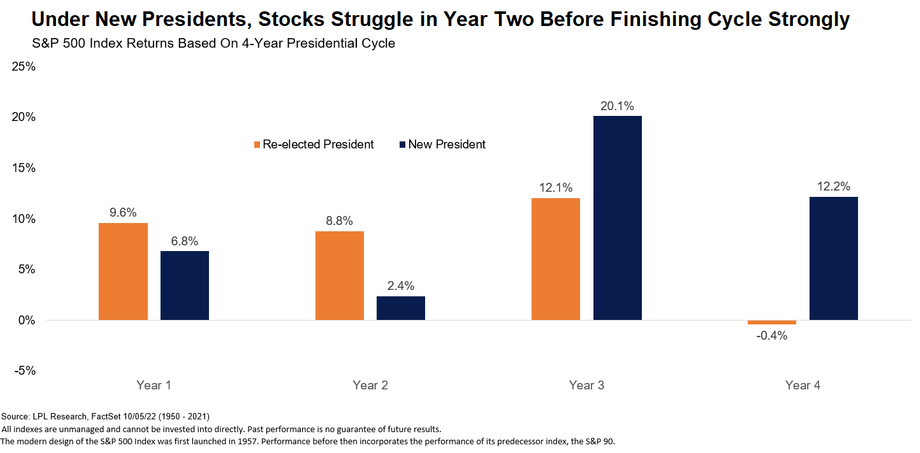

Related to the prior data but zooming out further on the Presidential cycle, we are also at point where historic trends have been a tailwind for stocks. Under new Presidents, markets have historically struggled in the second year, coming into the midterms, before seeing strong returns in the second half of the presidential cycle. Year three of a new President’s term has seen the best annual returns of the periods studied back to 1950, posting an average gain of 20%.

All of this data is based on historic trends and, of course, past performance is no guarantee of future results, but the fact that these trends, that appear to be tailwinds for stocks, have persisted, on average, throughout periods of high inflation, rising interest rates and recession is worth noting.

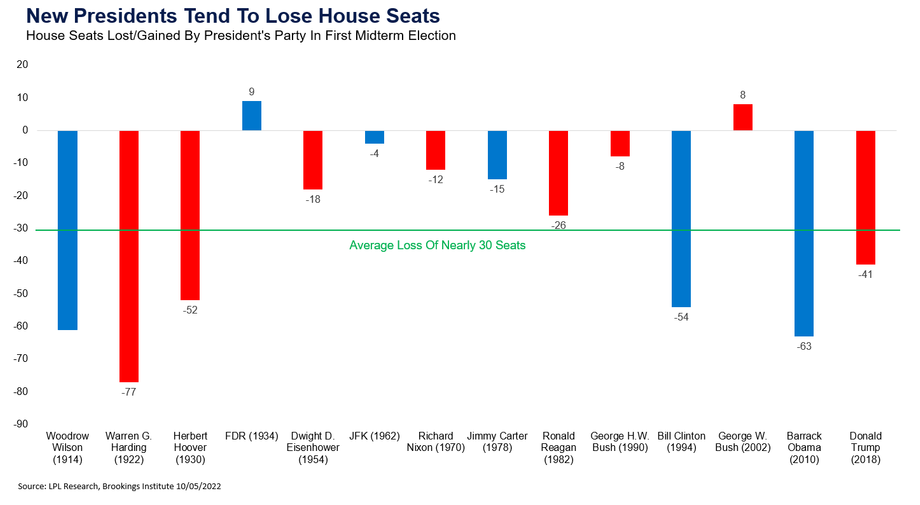

Having looked at the market related data, what does history tell us about the actual election? Looking back to 1914, new Presidents have tended to lose house seats in their first midterm election, with an average loss of almost 30 seats. Only twice have new Presidents actually gained house seats and, based on current polls, it doesn’t look likely 2022 will buck that trend.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data from FactSet and MarketWatch.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking # 1-05333024

For a list of descriptions of the indexes and economic terms referenced in this publication, please visit our website at lplresearch.com/definitions.