Posted by Jeffrey Buchbinder, CFA, Chief Equity Strategist

Wednesday, June 14, 2023

Now that the S&P 500 Index has entered a new bull market (by gaining 20% or more since the October 2022 lows), it’s logical to ask the question of when the index might achieve a new all-time high.

At 4,369 on the S&P 500 as of the market close on June 13, 2023, the index is just 9.8% away from eclipsing the record high from January 3, 2022 at 4,796.56. So how long might it take us to get there?

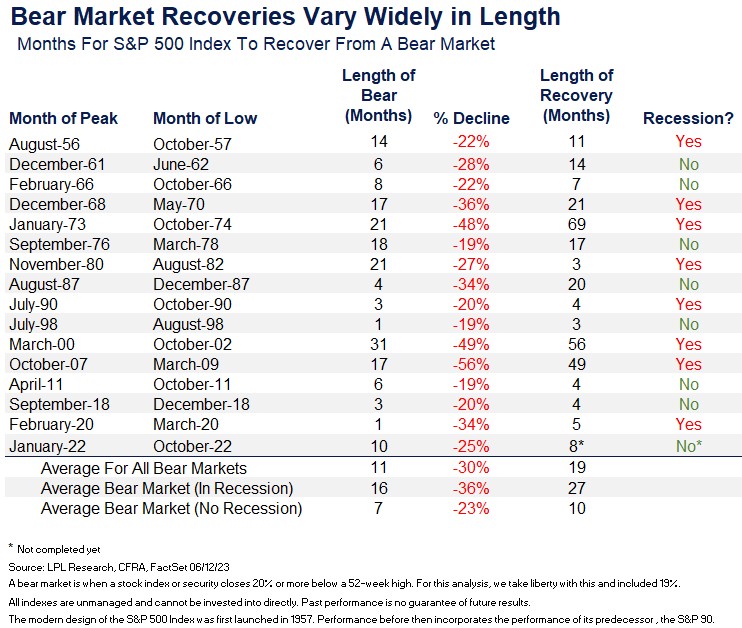

Historically, the index has taken an average of 19 months to recover from bear market declines of 20% or more, as shown in the accompanying table. The current rebound from the bear market low in October 2022 is now just eight months old, suggesting an additional 10% gain could potentially take almost another year to achieve.

As shown above, recovery times vary widely and depend on the economic environment. When bear markets are not accompanied by recession, recoveries from bear markets only took an average of 10 months to reach a new record high. It might be going out on a limb to predict a 10% rally and a new record high for the S&P 500 by mid-August, but the historical pattern for young bull markets suggests stocks may have some more room to run here. Perhaps the lack of a recession in this environment (so far, at least) means the timetable to return to the January 2022 highs could be closer to 10 months than 19. On the other hand, if recession begins this fall, before those new highs are reached, it could be well into 2024 before the S&P 500 eclipses the 4,796 mark.

This analysis doesn’t change the LPL Research Strategic and Tactical Asset Allocation Committee’s (STAAC) neutral stance on equities from a tactical asset allocation perspective. The STAAC still sees the risk-reward between equities and fixed income as fairly balanced currently, even while acknowledging this analysis points to more gains over the rest of the year. As we wrote about here in last week’s Weekly Market Commentary, the technical evidence that stocks may be due for a pause, coupled with the attractiveness of fixed income relative to equities, suggests it is prudent to keep portfolio risk levels near benchmarks, with a bit of an additional fixed income cushion to help mitigate potential equity market volatility and enhance income. Also, consider the possibility that lower interest rates enhance bond returns, consistent with the end of prior Federal Reserve rate hiking cycles.

In conclusion, with bonds offering some of the richest yields in decades, the risk-reward for stocks is no longer compelling, in our view. Strong momentum may carry the market a bit higher from here, but with the S&P 500 within our fair value range of 4,300 to 4,400, it seems like a logical spot for stocks to take a breather.

For more of LPL Research’s thoughts on the near-term outlook for stocks, see our latest LPL Market Signals podcast here.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data from Bloomberg.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking 1-05373345